How does this kit close the operational backbone an examiner expects?

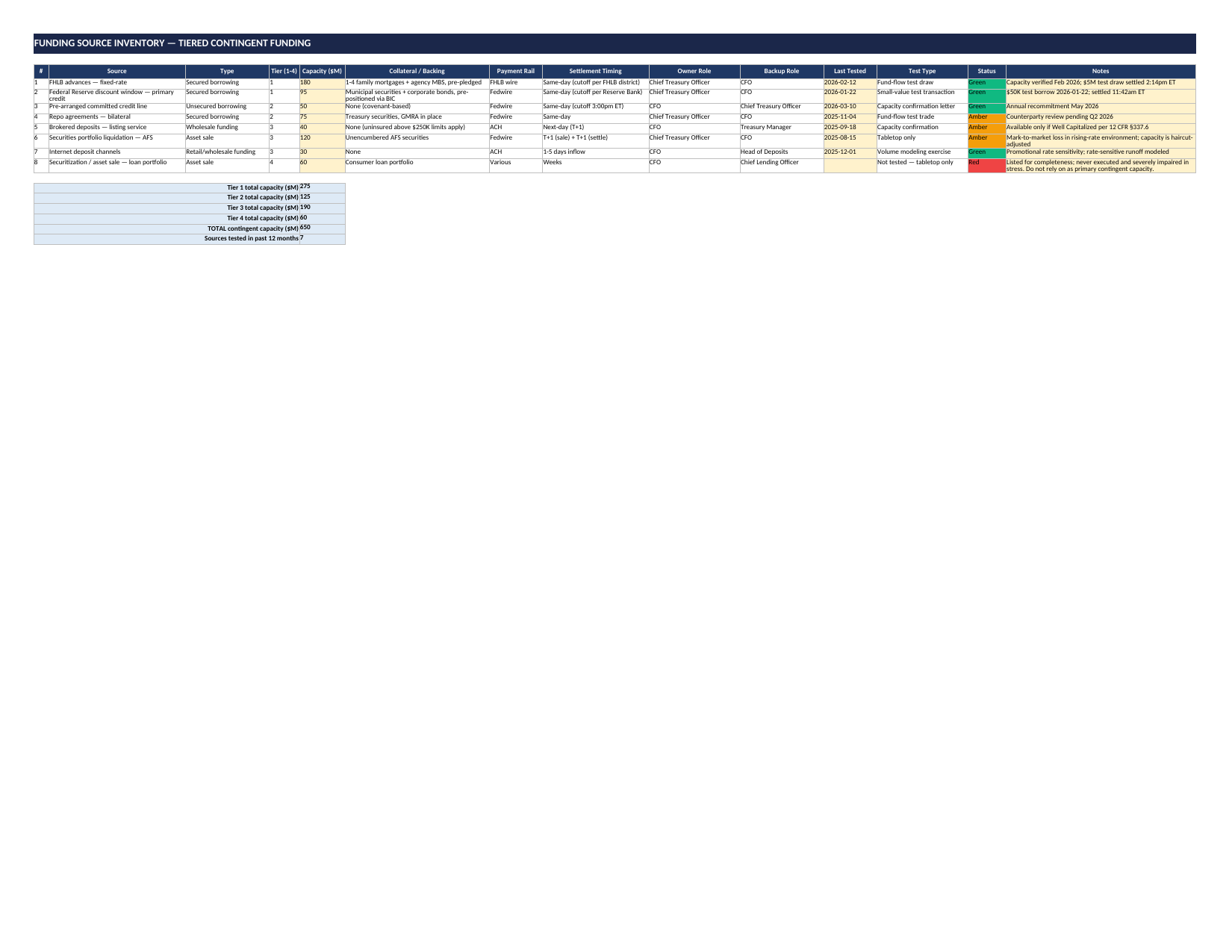

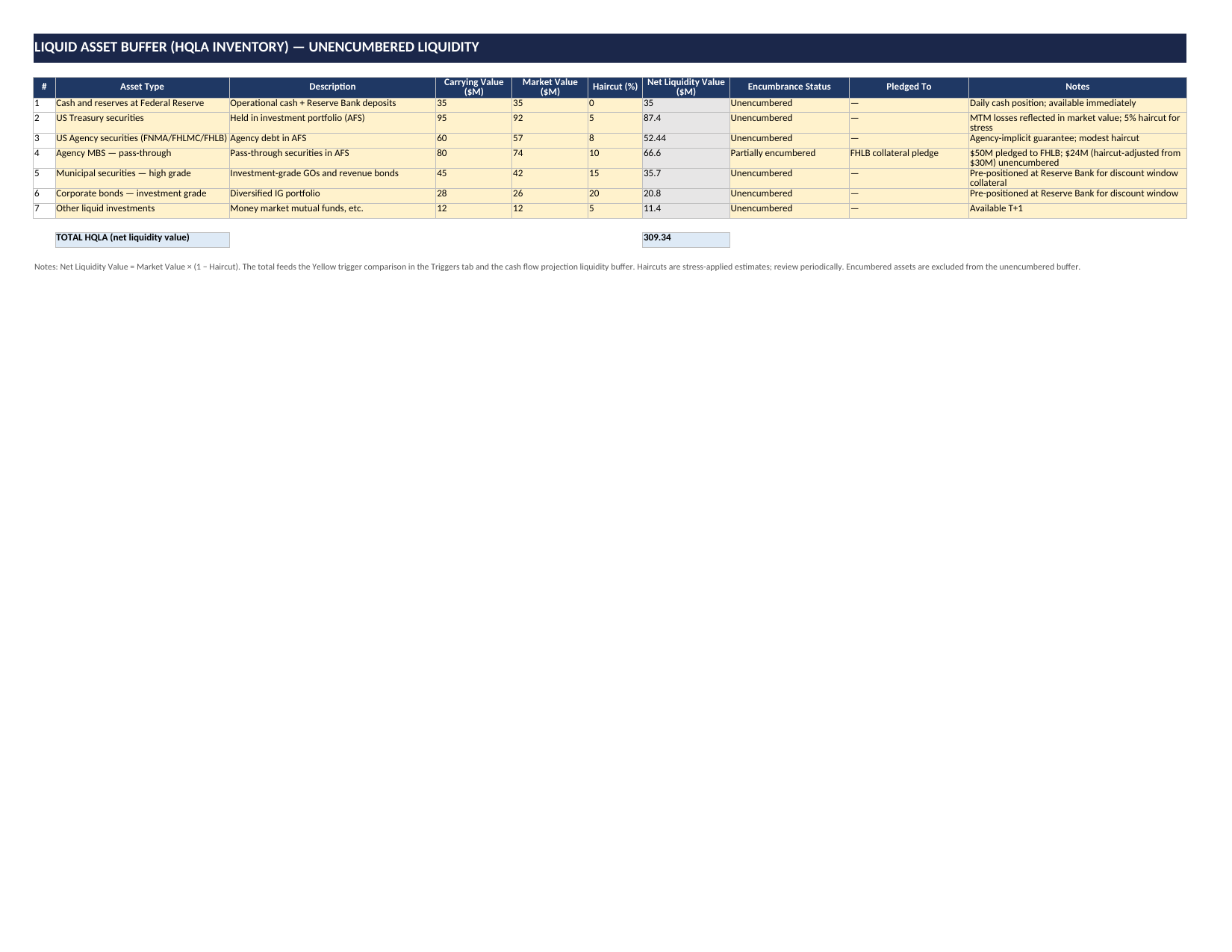

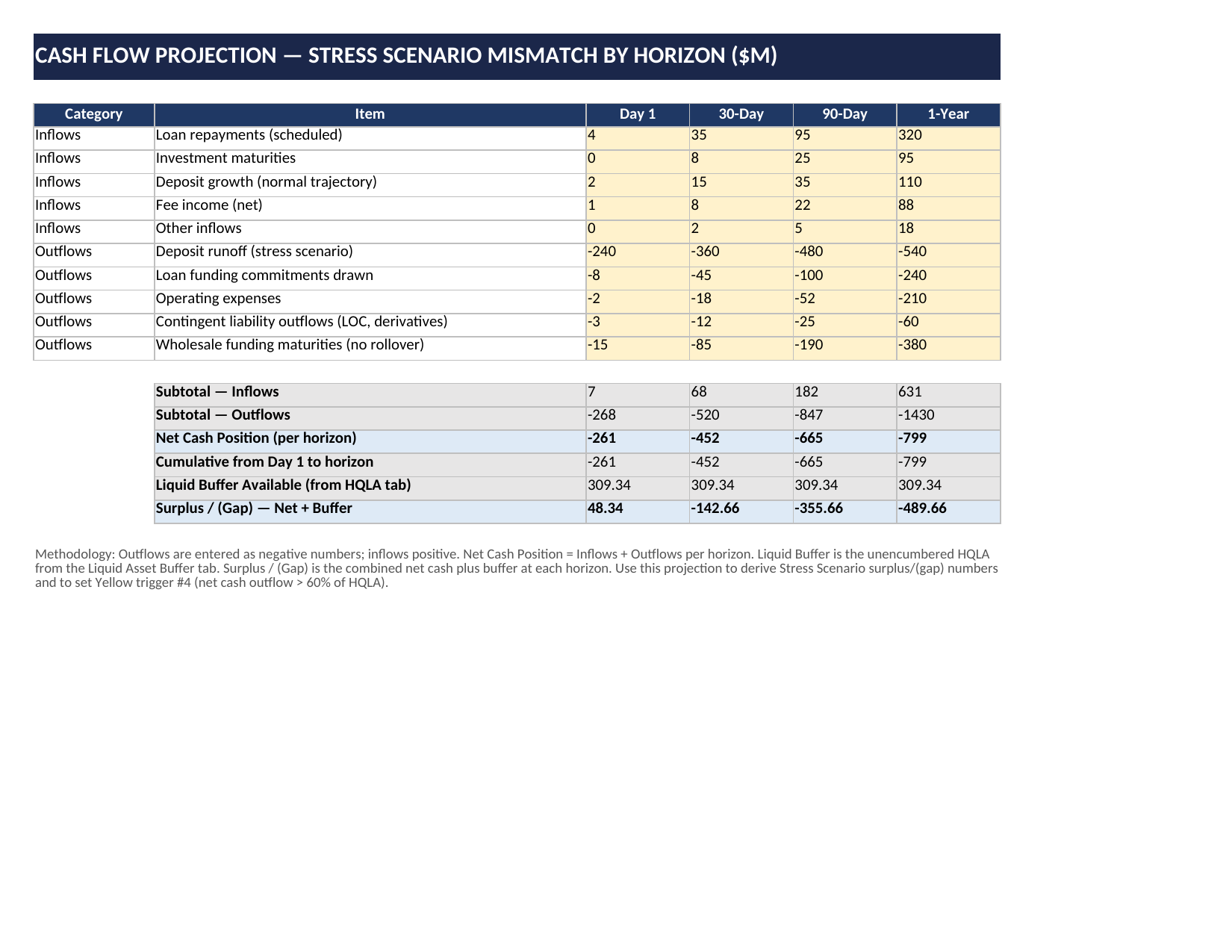

Most CFPs cover governance and triggers but skip the underlying math. This kit gives you the full operational backbone: a Liquid Asset Buffer (HQLA) inventory with stress-applied haircuts, a Cash Flow Projection across overnight/30/90/365-day horizons that derives your surplus/(gap), a Contingent Liabilities inventory (the IPS-contemplated component most CFPs underweight), an Assumptions Log documenting every input with rationale and CRO sign-off, and an Activation Playbook with tier-specific 1hr/4hr/24hr action checklists. The numbers in your stress scenarios actually reconcile to the math, which is what examiners increasingly look for.

How does this differ from the Financial Risk Management Kit?

The Financial Risk Kit is broader (credit, liquidity, capital, concentration, market risk) and includes a basic Liquidity Monitor tab. This CFP kit is purpose-built for the specific examiner expectation around contingency funding — the full operational backbone (HQLA buffer, cash flow projection, contingent liabilities, assumptions log), the trigger framework, the scenario library with worked math, the testing program, evidence binder, activation playbook, board reporting, and 24-paragraph policy language library. If you only need liquidity monitoring, the Financial Risk Kit covers it. If you need to defend your CFP to OCC, FDIC, or Federal Reserve examiners post-2023, this is purpose-built for that.

Is this calibrated for community banks or larger institutions?

The worked example uses Midwest Community Bank, $1.2B total assets — the asset threshold where examiner expectations sharpen materially. The structure is portable across $500M-$10B community and mid-size chartered banks. The kit includes a Modified LCR methodology callout designed for community banks under the $50B asset threshold (not directly subject to 12 CFR Part 249) but using LCR-style internal monitoring against Board-approved thresholds. Institutions at $50B+ subject to the full LCR rule can still use the kit's structure, but should treat the Modified LCR methodology as supplementary internal monitoring.

What are the six pre-built stress scenarios?

S1 — SVB-illustrative uninsured deposit run (idiosyncratic). S2 — Market-wide wholesale funding freeze (market). S3 — Combined idiosyncratic + market worst case (the regulator-recognized overlay used in large-bank rules and adapted proportionately for community/mid-size banks). S4 — Credit rating downgrade triggering PCA loss of brokered deposit access per 12 CFR §337.6. S5 — Operational/cyber disruption blocking cash mobility (CrowdStrike-illustrative). S6 — Concentrated deposit outflow from a single segment. Each scenario exposes deposit runoff, asset haircut, and surplus/(gap) cells as editable inputs that link back to the Cash Flow Projection.

What's an "Assumptions Log" and why does it matter?

The most common stress-testing finding is "unrealistic assumptions" — deposit runoff rates, haircuts, or funding availability that 2023 experience proved to be friendlier than reality. The Assumptions Log tab is where every assumption gets documented with the rationale (historical data, peer experience, regulatory guidance), the value, the last review date, and the reviewer sign-off. Twelve assumptions are pre-populated for the worked example. It's the single most effective hedge against the unrealistic-assumptions finding, and it's a tab most community bank CFPs simply don't have.

What's in the Activation Playbook?

When a Yellow/Amber/Red trigger fires, what specifically happens in the first hour? The first 4 hours? The first 24 hours? The Activation Playbook tab answers those questions concretely — 15 sequenced actions across the three tiers, each with a named responsible role, the decision authority required (e.g., "CFO authority for Tier 1 draws up to $[X]M"), and the output/evidence to capture. Walking through this with leadership before a stress event surfaces gaps that desk review never will.

What does the Policy Language Library include?

24 drop-in paragraphs organized into six sections that mirror CFP document structure: (I) Governance & Approvals, (II) Funding Strategy & Sources, (III) Liquidity Risk Measurement & HQLA, (IV) Triggers & EWIs, (V) Testing & Evidence, and (VI) Activation, Crisis Management, and Review. Each paragraph has bracketed fill-in blanks and is written to survive examiner follow-up questions — every sentence answers an obvious next question.

What's a fund-flow test and why is it different from a tabletop?

A tabletop exercise tests decision-making — who decides to activate the CFP, how escalation works, what governance looks like. A fund-flow test tests execution — can you actually initiate the draw, move collateral, confirm receipt, and document settlement in the timeframe the CFP assumes? Both serve distinct purposes. The 2023 Addendum specifically pushed toward operational fund-flow testing — that's what the workbook's Testing Log captures with separate test-type values.

What does the 2023 Interagency Addendum actually say?

The Addendum (OCC Bulletin 2023-25, FDIC FIL-39-2023, issued July 28, 2023 after the regional bank failures earlier that year) sets out supervisory expectations that depository institutions maintain operational readiness to borrow from contingent sources — including conducting periodic transactions to test discount window access. The supervisory focus shifted from "describe your sources" toward "demonstrate tested access." A CFP that lists the discount window without a documented test record increasingly draws supervisory feedback at examination. This kit is built to that standard. Buyers should verify current supervisory guidance with counsel and their primary examiner.

Can I share completed outputs externally?

Yes. You can use completed outputs with auditors, customers, bank partners, regulators, and internal stakeholders. Customize the template for internal business use — just don't resell or redistribute the source template files.

How do I receive the files?

Checkout is handled through Stripe. After purchase, you receive the template and guide download link immediately on the confirmation page and by email, along with your Stripe receipt. No account is required.

What if it's not a fit?

Email within 30 days for a full refund, no questions asked. The guarantee is meant to remove purchase risk while you evaluate whether the template fits your use case.