Do fintechs without bank charters actually need a CFP?

You're not directly subject to OCC or FDIC CFP rules. But your sponsor bank is. Under the 2024 Interagency Joint Statement on Bank-Fintech Arrangements, sponsor banks are expected to understand and manage liquidity risks arising from their fintech programs. In 2024 the FDIC also issued a proposed rule (NPRM) on custodial-account recordkeeping for accounts holding consumer funds; that rule had not been adopted in final form as of the time this kit was prepared (verify current status with counsel). A fintech that cannot demonstrate liquidity resilience and disciplined FBO recordkeeping creates sponsor-bank program risk regardless of the final rule's status. Public reporting on the Synapse failure crystallized the operational cost of not having a tested CFP and disciplined FBO controls.

How does this kit close the operational backbone an examiner or sponsor bank expects?

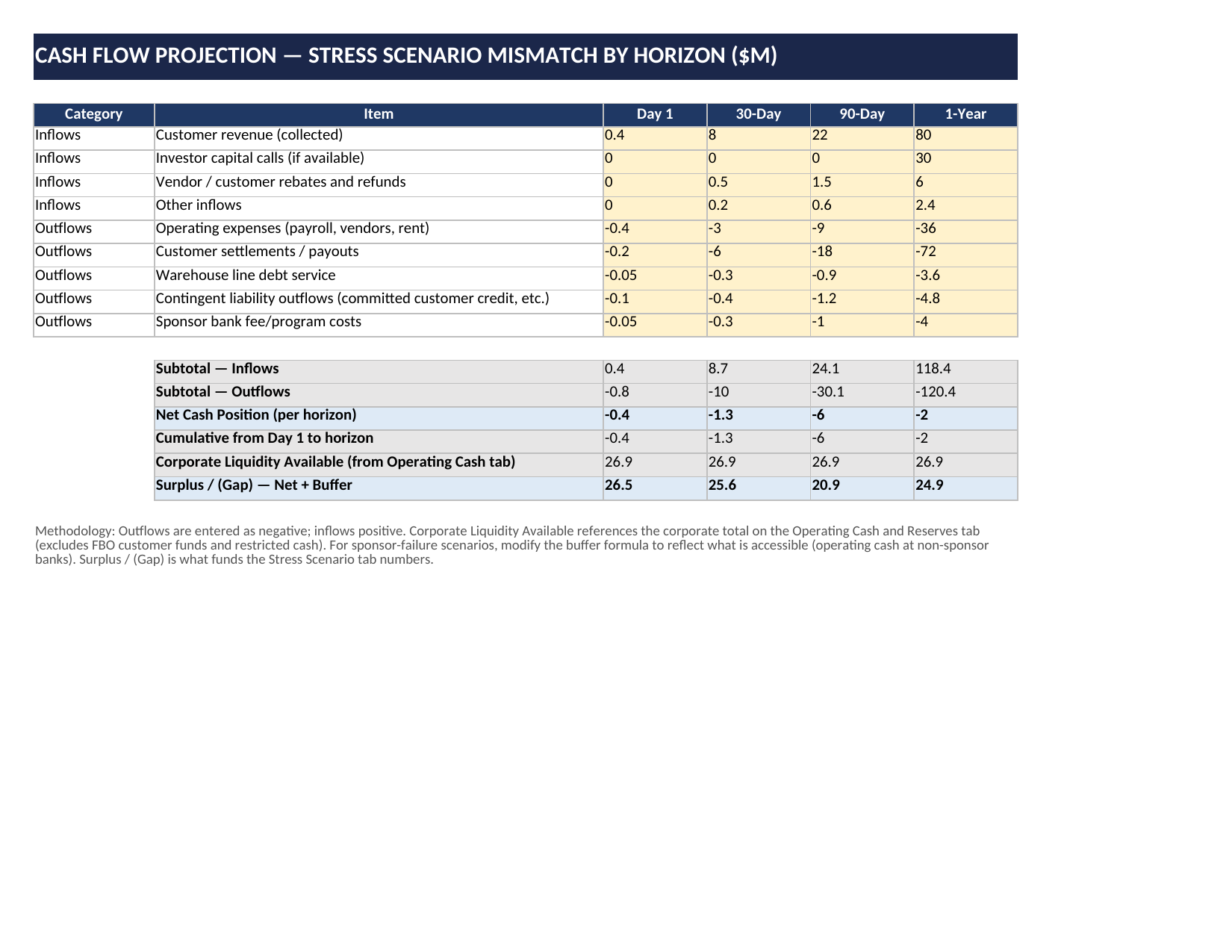

Most fintech CFPs cover governance and triggers but skip the operational backbone. This kit gives you: Operating Cash & Reserves inventory with strict corporate-vs-FBO segregation, Cash Flow Projection deriving stress scenario gaps, FBO Reconciliation as a recommended sponsor-bank readiness control, Assumptions Log documenting every input with CRO sign-off, and an Activation Playbook with tier-specific 1hr/4hr/24hr action checklists. The numbers in your stress scenarios actually reconcile to the math, and you have the controls evidence sponsors and examiners increasingly expect post-Synapse.

How are fintech CFPs different from bank CFPs?

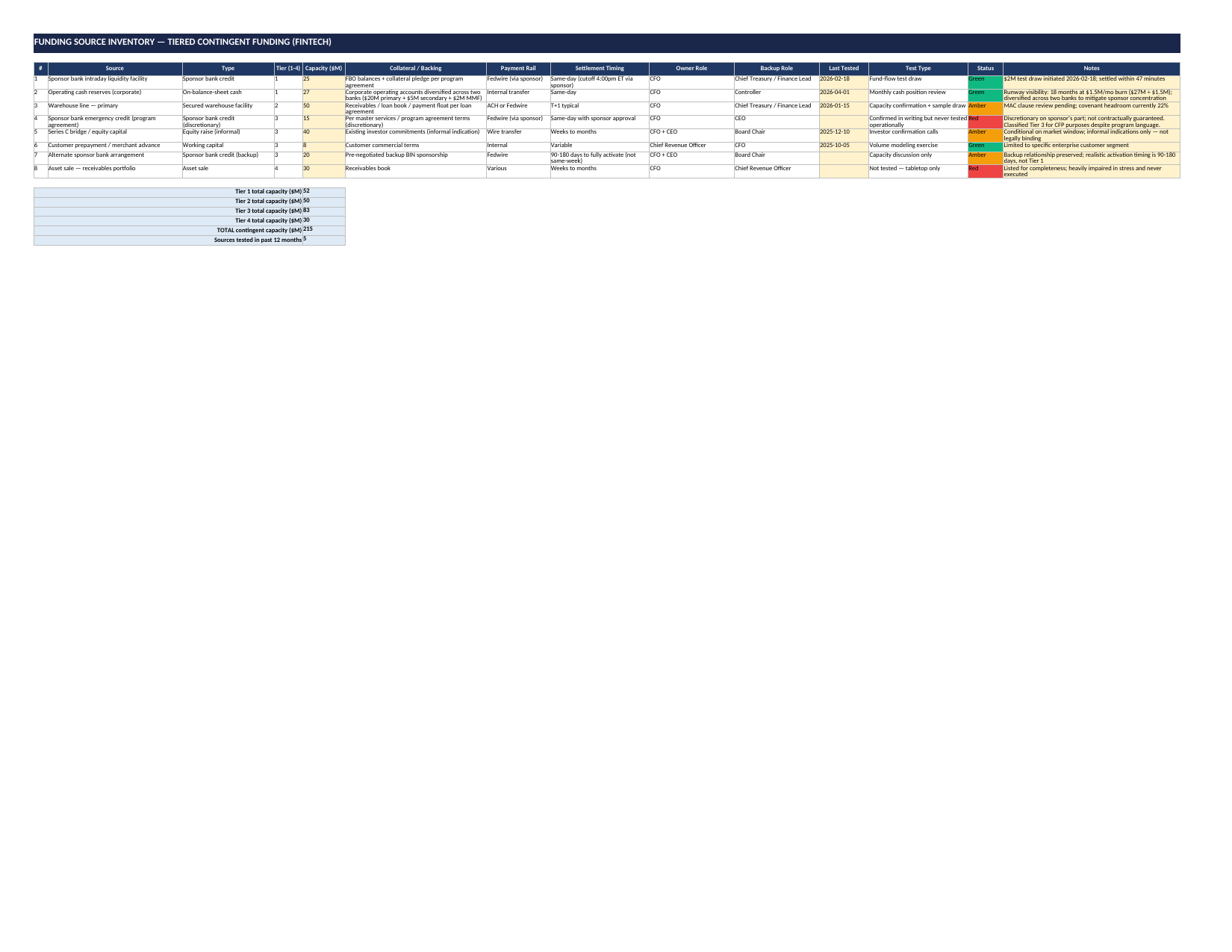

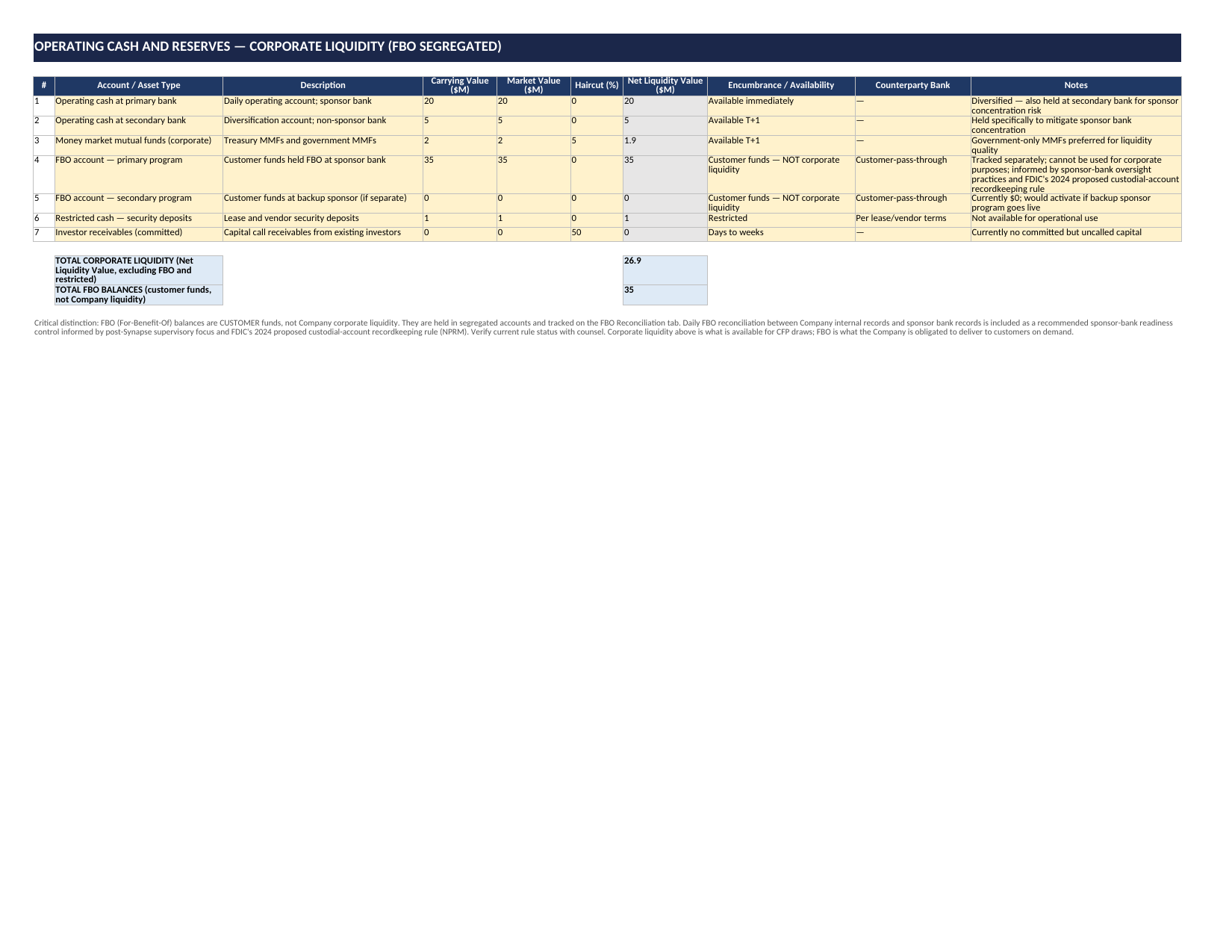

Funding sources are entirely different (sponsor bank credit, warehouse line, equity reserves, payment rails — not discount window, FHLB, brokered deposits). Metrics are different (runway and burn, not LCR/NSFR). Governance is different (CFO + CRO + Audit Committee, not three-line-of-defense with Treasury and ALCO). Stress scenarios are different (Synapse-illustrative sponsor failure and warehouse MAC, not SVB-illustrative deposit run). Customer funds handling is different (strict FBO segregation, daily reconciliation informed by FDIC's 2024 proposed custodial-account recordkeeping rule and sponsor-bank oversight practices). This kit is built specifically for sponsor-bank fintechs.

What does the FBO Reconciliation tab do, and why is it included as a key fintech CFP control?

The FBO Reconciliation tab implements daily reconciliation between the fintech's internal customer ledger and the sponsor bank's statement of FBO balances. It's included as a recommended sponsor-bank readiness control, informed by FDIC's 2024 proposed custodial-account recordkeeping rule (NPRM) and post-Synapse supervisory focus. The tab tracks variances by source, reason, reconciler/reviewer attestation, and Green/Yellow/Red variance thresholds tied to the Triggers tab. Whether or not the proposed FDIC rule lands exactly as drafted, daily reconciliation with documented variances and remediation is what sponsor banks and examiners increasingly expect.

What are the six pre-built fintech stress scenarios?

S1 — Sponsor bank failure or termination (Synapse-illustrative). S2 — Warehouse MAC-clause invocation. S3 — Customer-base concentration run (top 20 customers leave). S4 — Payment rail disruption (FedNow, ACH, or wire outage). S5 — Adverse regulatory action (supervisory action limiting transaction volume). S6 — Failed equity raise during runway-extension window. Each scenario exposes editable assumptions for customer attrition, sponsor response timing, warehouse covenant behavior, and market accessibility. S1 includes the critical corporate-vs-FBO distinction in the worked example.

What's the Activation Playbook?

When a Yellow/Amber/Red trigger fires, what specifically happens in the first hour? The first 4 hours? The first 24 hours? The Activation Playbook tab answers those questions concretely — 15 sequenced actions across the three tiers, each with a named responsible role, decision authority required, and output/evidence to capture. The Red tier sequence specifically addresses the sponsor bank failure scenario (alternate sponsor activation at the realistic 90-180 day timeline) and the FBO reconciliation material discrepancy scenario (outside counsel, sponsor escalation, and consideration of regulator notification consistent with applicable law and program agreement).

Why is the backup sponsor bank arrangement classified as Tier 3, not Tier 1?

Because backup sponsor activation realistically takes 90-180 days. Diligence, contracting, BIN sponsorship transitions, and customer comms all take time. A backup that takes six months to fully activate is not a same-week contingent source — treating it as Tier 1 creates false confidence. The kit explicitly flags this as one of the most common sponsor bank program review findings, and the Assumptions Log documents the 90-180 day timing with rationale.

When would I share my CFP with my sponsor bank?

Proactively, during program reviews, and in response to liquidity Requests for Information (RFIs). The 2024 Joint Statement creates an expectation that sponsor banks understand fintech liquidity. Sharing your CFP shifts the dynamic from bank-driven RFI to fintech-driven assurance — which strengthens the program relationship and reduces examination friction. The kit includes Policy Language Library paragraphs specifically on sponsor bank coordination and the FBO Reconciliation tab evidence is what sponsors want to see during program reviews.

What does the Policy Language Library include?

24 drop-in paragraphs organized into six sections that mirror CFP document structure: (I) Governance & Approvals (including 2024 Joint Statement language), (II) Funding Strategy & Sources, (III) Operating Cash, FBO Segregation & Reconciliation (with language framed around the FDIC 2024 proposed custodial-account recordkeeping rule and sponsor-bank readiness expectations), (IV) Triggers & EWIs, (V) Testing & Evidence, and (VI) Activation, Crisis Management & Review (including sponsor bank failure protocol). Each paragraph has bracketed fill-in blanks and is written to survive sponsor bank, audit committee, or examiner follow-up. Buyers should verify current rule status and consult counsel before relying on specific regulatory citations.

Can I share completed outputs externally?

Yes. You can use completed outputs with auditors, customers, bank partners, regulators, and internal stakeholders. Customize the template for internal business use — just don't resell or redistribute the source template files.

How do I receive the files?

Checkout is handled through Stripe. After purchase, you receive the template and guide download link immediately on the confirmation page and by email, along with your Stripe receipt. No account is required.

What if it's not a fit?

Email within 30 days for a full refund, no questions asked. The guarantee is meant to remove purchase risk while you evaluate whether the template fits your use case.