How is this different from a generic AUP template?

A generic AUP gives you a list of prohibited industries. This kit gives you the operational backbone: a Sales-facing intake questionnaire that auto-routes deals (so Sales velocity stays intact), a documented approval path (so reviews don't get improvised), a Bank Partner Alignment matrix (because your sponsor bank's rules are the binding constraint), an Exception Memo template with the 10 elements an examiner expects, a post-approval monitoring library with default thresholds, and a populated Worked Example showing the full lifecycle. The PDF guide includes 28 drop-in policy paragraphs you can paste into your own AUP document.

Do I have to run every customer through this?

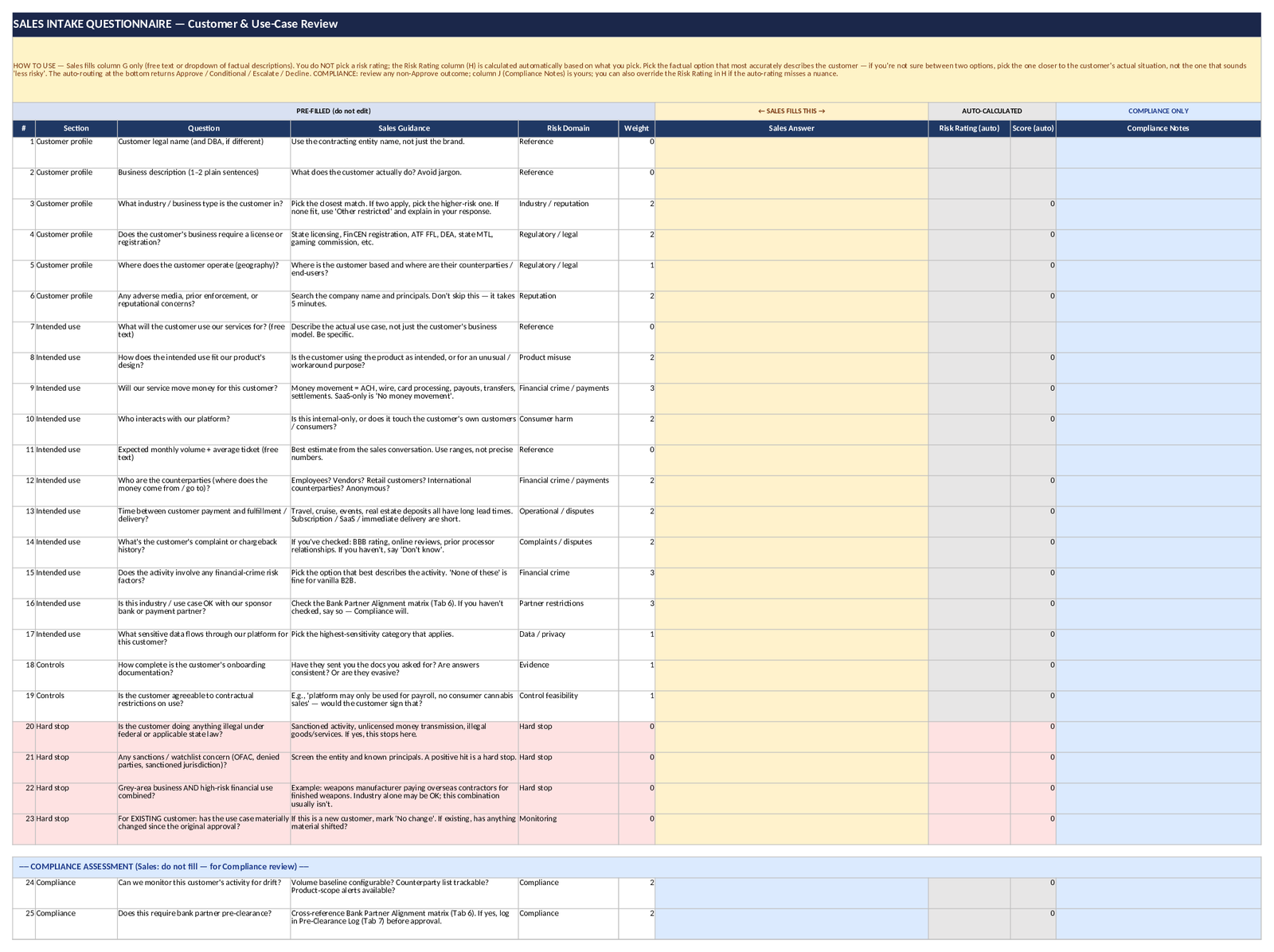

No — and that's the point. The Sales Intake Questionnaire is designed so 80–90% of standard deals get an "Approve" output and proceed to onboarding without compliance review. Only deals that score Conditional / Escalate / Decline route to Compliance. The structured questions ensure that when a deal does need a deeper look, Sales has captured the right facts up front — Compliance doesn't re-ask the same questions.

Is this fintech-specific or for banks too?

This v1 is built for fintechs (BaaS programs, sponsor-bank arrangements, payment platforms). The bank-partner alignment, RFI KRI tracker, and the regulatory anchor all reflect the 2024 BaaS enforcement cycle and the Aug 2025 Debanking EO. A banks edition (correspondent-bank-focused, card-network-aligned) is planned separately.

What does the worked example show?

GreenLeaf Payroll — a fictitious licensed Colorado cannabis retailer that wants to use the platform for payroll only (no consumer cannabis sales touch the platform). The example walks through: Sales Intake Questionnaire output, Compliance EDD findings, sponsor bank pre-clearance with conditions (cap, license re-verification, notification), the populated Exception Memo, monitoring baselines set at approval, a six-month volume-drift trigger event with documented investigation and memo update, and the annual re-review with cap increase. Every artifact in the kit is populated so you can see the full lifecycle.

How does the Bank Partner Alignment Matrix work?

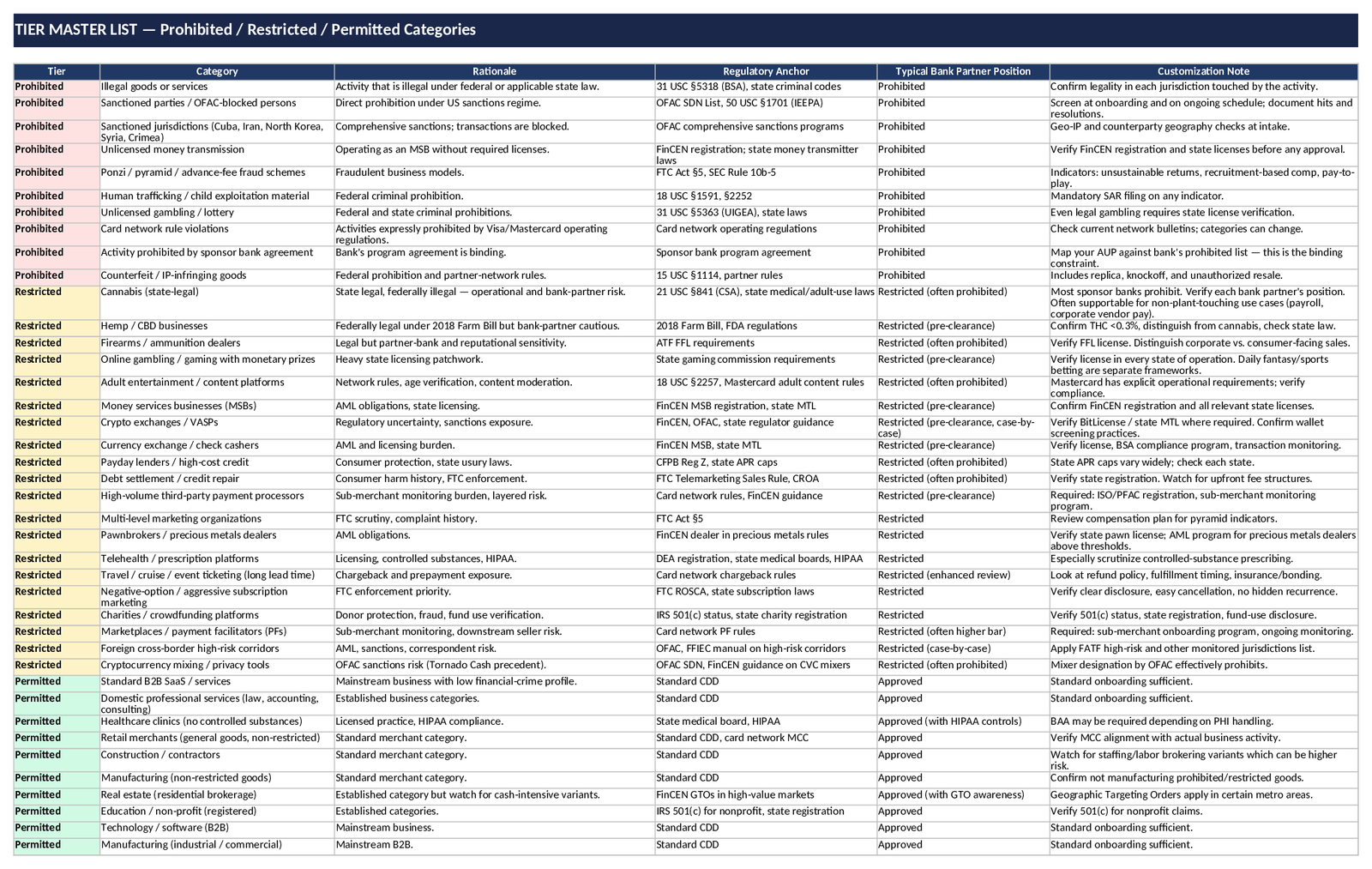

For each of 20+ seeded restricted categories, you enter your AUP position (Prohibited / Restricted / Permitted) and your sponsor bank's position (from the program agreement). The Gap column auto-calculates: Aligned (positions match), Gap (positions differ — manageable direction), or Material Gap (your AUP is more permissive than the bank's — the dangerous direction). Material Gaps must be addressed before any further onboarding in that category. The matrix is reviewed annually and whenever the bank updates its program requirements.

Does the kit include the Exception Memo template?

Yes — Tab 8 of the workbook. The memo has 10 sections matching the FFIEC BSA/AML manual's EDD documentation expectations: Customer Identification, Business Category & AUP Classification, Platform Use & Transaction Types, Fund Flow Description, Prohibited/Restricted Analysis, Applicable Controls, Monitoring Plan & Review Schedule, Bank Partner Status, Approval & Sign-Off, and Exit Triggers. The memo is fillable; one customer per memo. The Worked Example tab shows how a populated memo looks.

How does the RFI Volume KRI Tracker work?

Track monthly RFIs from your sponsor bank by customer category. The workbook auto-calculates cumulative YTD and a Rising / Stable trend indicator (formula-based comparison to 3-month average). Rising RFI volume in a specific category is the structural early warning of bank partner discomfort — the pattern that preceded the 2024 BaaS consent orders. Escalate Rising trends to TPRM governance before they become formal warnings.

How does this fit with KYC and AML programs?

The AUP decides whether the customer or activity is eligible. KYC/CDD decides how closely you review the relationship. Transaction monitoring decides what you flag in ongoing activity. This kit is the AUP layer — it tells you whether you should onboard the customer at all, and what conditions and monitoring apply if you do. KYC/CDD and transaction monitoring sit downstream.

Can I share completed outputs externally?

Yes. You can use completed outputs with auditors, customers, bank partners, regulators, and internal stakeholders. Customize the template for internal business use — just don't resell or redistribute the source template files.

How do I receive the files?

Checkout is handled through Stripe. After purchase, you receive the template and guide download link immediately on the confirmation page and by email, along with your Stripe receipt. No account is required.

What if it's not a fit?

Email within 30 days for a full refund, no questions asked. The guarantee is meant to remove purchase risk while you evaluate whether the template fits your use case.